Interest rates on most savings and checking accounts remain anemic. But for those who are comfortable with electronic banking and who are active debit-card users, high-yield checking accounts offered by smaller, regional banks and credit unions can be a more lucrative option.

The financial site Bankrate.com examined 56 “high yield” checking accounts across the country, and found an average yield of 1.64 percent. That’s considerably lower than rates the site found last year. But it looks quite good in comparison to most interest-bearing checking accounts, which had a national average yield of just 0.05 percent.

The catch is that to benefit from the accounts, which are federally insured, users have to meet some requirements each month.

For instance, all of the accounts reviewed by Bankrate require at least 10 debit-card transactions a month, and all require that users receive their monthly statements electronically. Most also require direct deposit or automated bill payments.

The penalty for not meeting the requirements is severe — the average interest rate drops to just 0.07 percent.

If 10 debit transactions are required a month and you make just nine, you’re out of luck, said Greg McBride, senior analyst at Bankrate.

In addition, the accounts all carry balance caps — maximum balances on which the above-market interest rate applies.

The average cap is about $17,000 (down from about $19,000 last year), but the highest-yielding accounts tend to have the lowest caps. None of the 14 best-paying accounts available nationally, for instance, have a cap above $15,000, so if you had $20,000 in the account, the additional $5,000 would not earn the higher rate.

Still, Mr. McBride notes, consumers who can handle the requirements may still benefit from the accounts, perhaps as a place to park emergency funds or other cash.

Roughly a third of the high-yield accounts that Bankrate surveyed are available nationally, although some require a visit to a branch to open the account. About 39 percent of the accounts have some geographic limitation, like in-state residency.

Ouachita Independent Bank in Monroe, La., for example, offers a 3.01 percent annual percentage yield — but the account is available only to residents of Louisiana, Texas, Arkansas and Mississippi.

Do you have a high-yield checking account? Do you find it easy to meet its requirements?

Article source: http://bucks.blogs.nytimes.com/2013/06/03/finding-a-high-yield-checking-account/?partner=rss&emc=rss

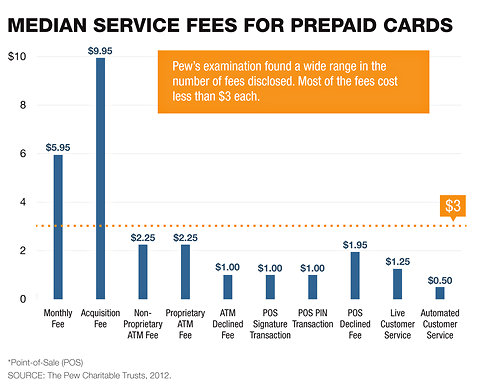

Bucks: Pew Feature Illustrates Banks’ Transaction Infractions

An arm of the Pew Charitable Trusts have been gaining some traction with its campaign to get banks to disclose fees associated with checking accounts in clear, simple language. One bank practice that Pew thinks is especially important for banks to clearly explain is the order in which they process transactions, which can affect the number of fees you pay if you overdraw your account.

To help illustrate the problem, Pew’s Safe Checking in the Electronic Age project has created an interactive feature, dubbed “Transaction Infraction.” The tool lets you toggle between two screens that show you how the way in which a bank orders your transactions can greatly increase the fees you will pay. (The example is taken from an actual court case, Gutierrez vs. Wells Fargo Bank).

On the first screen, you can see what happens when the 12 transactions were processed chronologically. Mr. Gutierrez ends up with a negative balance of about $45, and a single $22 fee.

On the second screen, you can see the order in which Wells Fargo actually processed the same transactions. The result is a negative balance of nearly $112, and four fees, totaling $88.

Banks have typically processed transactions in the order of the largest to the smallest, which can increase overdraft fees. But some banks are now switching to processing the smallest , or at least chronological order.

(Wells Fargo made changes last May to the way it processes some payments. Paper checks and automatic deductions — like pre-authorized monthly student loan payments — are still paid from high to low. But the bank processes A.T.M. withdrawals, debit card purchases and online bills chronologically, in the order received.)

Take a look at the tool and let us know what you think in the comments section.

Article source: http://feeds.nytimes.com/click.phdo?i=ebdea140ad1b5e0e97942a5162ac6b7e