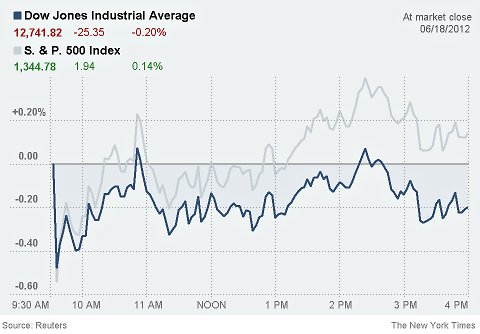

In the end, stocks on Wall Street closed mixed on Monday, after a mini-roller-coaster ride first down, then up, then a little sideways, leaving Sunday’s critical Greek elections with a so-so endorsement.

The Dow Jones industrial average closed down about 25 points, or 0.2 percent, while the Standard Poor’s 500-stock index added around 2 points, or 0.1 percent. The Nasdaq composite index rose a strong 0.8 percent.

It was the bond market that voted “no” at the end of the day, with yields on Treasury securities staying at low numbers and yields on euro zone debt rising. The 10-year Spanish bond ended the European day with a surge to 7.125 percent, and the Italian 10-year yielded 5.915 percent.

As the euro zone dodges one minefield, it faces the larger question of whether European leaders can find a more lasting solution to an economic debacle now well into its third year. Jack Ewing, Nicholas Kulish and Paul Geitner take a look at the growing list of problems as the heads of European Union member governments prepare to meet next week in Brussels.

In Greece late Monday, the leader of the moderate Democratic Left party, Fotis Kouvelis, indicated that his party might be ready to join a coalition. In a televised statement after his meeting with Antonis Samaras of New Democracy, he emphasized the need “for a government, and a progressive one, to lead the country out of deadlock.” He did not refer once to the leftist party Syriza, which he had insisted should form part of a coalition after the inconclusive elections in May.

Mr. Kouvelis called on other parties to respond to the conditions for cooperation that he had set out before the elections, including extending the duration of Greece’s fiscal adjustment program and abolishing laws like the reduction of the minimum wage. He also called for immediate negotiations aimed at “disengaging from the onerous terms” of the bailout.

Mr. Samaras, for his part, said he had had “a constructive discussion” with Mr. Kouvelis and that talks would continue on Tuesday.

– NIKI KITSANTONIS, Athens

Crude prices have declined to an eight-month low in the last week from a high of around $110. One reason, in general, is that markets have been pricing in the prospects of slowing growth in Asia, especially China, which would reduce demand.

Approaching the end of the trading day on Wall Street, the industry that has been hit the hardest is energy. As crude prices fell, the Standard and Poor’s index tracking those stocks was down about 1 percent after 2 p.m. Financials were next, down about 0.4 percent.

The news from Europe after the Greek election showed that there was still uncertainty. Spanish bond yields up around 7 percent suggested that getting access to credit markets would be difficult. Bond yields also soared in Italy.

Gene McGillian, a broker and analyst at Tradition Energy, said the results of the Greek elections did little to eradicate the fears over the euro zone debt problems, and traders have refocused on uncertain economic conditions.

“There is still uncertainty there,” he said. “The problems in the euro zone are still simmering.”

He said the oil markets were also pricing in inconsistent data from the United States, where oil stocks are already high.

“That is why we dropped down to about $80,” he said.

– CHRISTINE HAUSER, New York

Are the leaders of the European Union bracing for a barrage of criticism as a meeting of the Group of 20 gets under way in Los Cabos, Mexico?

It certainly sounded like it on Monday at a news conference, where officials took the offensive over the origins of the economic crisis and the difficulties of pushing through structural changes quickly.

“This crisis was originated in North America, and many of our financial sectors were contaminated by, how can I put it, unorthodox practices from some sectors of the financial market,” said Jose Manuel Barroso, the president of the European Commission, the union’s executive agency.

“Frankly, we are not coming here to receive lessons in terms of democracy or in terms of how to handle the economy,” said Mr. Barroso.

Instead of criticism, Mr. Barroso said, he wanted to hear approval from other G-20 leaders for the efforts being made in Europe, especially in view of the public opposition to austerity measures in countries like Greece.

Herman Van Rompuy, the president of the European Council, the body that represents European Union heads of state and government, also seemed to begin a pre-emptive strike against finger-wagging at the conclave in Mexico.

“We are correcting internal imbalances, and a lot of other countries have to correct their huge external imbalances,” said Mr. Van Rompuy. “So we are not the only ones who are so-called responsible for the current economic problems all over the world.”

That Europe needed to take into account its citizens’ opinions also was a factor the rest of the world should appreciate, said Mr. Van Rompuy. ”Undertaking reforms in a democracy is much more difficult than in other regimes — I put it mildly,” he said.

– JAMES KANTER, Brussels

The euro zone will move quickly on a deal for a banking union, an element of deeper economic integration among countries that use the single currency and one that would entail combined banking supervision, the president of the European Council, Herman Van Rompuy, said on Monday.

“The priority is given to the banking integration and, in the bank integration, I think we can reach, sooner than in other matters, an agreement on a more centralized and more common supervision,” Mr. Van Rompuy said in a news conference in Mexico before of the Group of 20 meeting, according to a report from Reuters.

He said a banking union was likely to be possible faster than other elements of deeper integration, such as a fiscal union or joint debt issuance, adding that it would be possible if no treaty change was required.

He also stressed that, while euro zone leaders would not make final decisions on anything at their next summit at the end of June, the decision to go ahead with further economic integration was more important than the pace of it.

“The most important thing is that we show the willingness to correct the weakness of the policy infrastructure of the common currency,” Mr. Van Rompuy said. “Even if in June we don’t take definitive decisions, the path, the trajectory, is very clear for everybody.”

President Obama, in Mexico on Monday, echoed the sigh of temporary relief coming from global leaders over the outcome of Greece’s elections, cautiously calling it a “positive” opportunity for the crisis-torn country to form a government.

But in a sign of just how fragile the Greek economic situation remains – and just how slender the margin of victory was for the pro-Europe backers in Athens – Mr. Obama couched his words with what seemed a veiled appeal to Germany to ease up on its austerity-first demand for how Greece should handle its fiscal crisis.

“I think the election in Greece yesterday indicates a positive prospect for not only them forming a government, but also them working constructively with their international partners in order that they can continue on the path of reform and to do so in a way that also offers the prospects for the Greek people to succeed and prosper,” Mr. Obama said, in remarks before an economic summit of world leaders here.

– HELENE COOPER, San Jose del Cabo, Mexico

Andrea Comas/ReutersCristóbal Montoro, the Spanish treasury minister.

Andrea Comas/ReutersCristóbal Montoro, the Spanish treasury minister.

Although Spain’s cost of borrowing — over 7 percent for 10-year bonds — is now about the level that caused Greece and Ireland to consider themselves locked out of the markets and ask for international bailouts, Spain has a much lower overall debt load than those two countries.

And as a bigger country, it can probably sustain higher interest rates for a longer period than smaller countries can, since any one bond auction will make up a relatively small percentage of its debt portfolio.

Spain is set to test the markets further this week by auctioning about 5 billion euros of debt. On Tuesday, the Treasury plans to sell as much as 3 billion euros in bills, and a bond sale on Thursday is intended to raise up to 2 billion euros.

On Monday, the Spanish treasury minister, Cristóbal Montoro, urged the European Central Bank to act to support the markets.

‘‘The E.C.B. must respond firmly, with reliability, to these market pressures that are still trying to derail the joint euro project,’’ he told the Spanish Senate during a budget hearing.

There was no immediate response from the European Central Bank in Frankfurt. But, often, pressure from politicians can cause the central bank to hold back, rather than appear to be influenced. Last week, the president of the bank, Mario Draghi, said it stood ready to react to market turbulence if necessary.

The yield on the 10-year debt of Italy, a country that is also on many financial analysts’ watch lists, tiptoed back over 6 percent on Monday.

– RAPHAEL MINDER, Madrid

On the Economix blog, Floyd Norris wonders whether the election with real impact on Europe on Sunday might have been the one in France.

Evangelos Venizelos, head of the socialist Pasok party, called for “as broad a coalition as possible” to be formed by Tuesday night.

After talks with the leader of the victorious New Democracy party, Antonis Samaras, Mr. Venizelos also condemned the leftist leader Alexis Tsipras for showing an “irresponsible” and “politically provocative” stance by insisting on remaining in opposition to a coalition.

“We agreed that the country must have a government immediately,” Mr. Venizelos said about his talk with Mr. Samaras. “Ideally, we would have a government by tomorrow night.”

In view of Mr. Tsipras’s refusal to join a coalition – which Mr. Venizelos described as “an antidemocratic, threatening” stance – he accused Mr. Tsipras of “trying to create the conditions for the failure of the government, the failure of the country.”

Updated | 1:07 P.M.

Panos Kammenos, the head of the right-wing antibailout party Independent Greeks, said he would not join a coalition since Mr. Samaras did not guarantee renegotiation of the bailout terms or that Greece would not default.

“That was it for us,” he said after talks with the conservative leader.

Mr. Kammenos said his party would support only legislation that would help Greece escape “the clutches” of the country’s foreign creditors.

Of Mr. Kammenos, Mr. Samaras said, “He does not understand the urgency of the situation.”

Mr. Samaras is to meet Democratic Left leader, Fotis Kouvelis, at 8.30 p.m. local time, the last scheduled meeting of the evening.

– NIKI KITSANTONIS, Athens

Even though concerns over the Greek election results seem to have receded somewhat, there was still enough worry in the world to keep the United States Treasury bond market behaving like a safe haven.

Yields were about even at 1.562 percent at midday on the benchmark 10-year bond.

The election results, said Tobias Levkovich, chief United States equities strategist of Citigroup, removed an imminent crisis, but Greece still has to form a coalition government to negotiate the debt problem. Spain is also still a worry.

“Clearly Wall Street preferred this outcome, ” he said. But he added, “we have not resolved the core problem, which is the need to ensure that countries can pay back their debt.”

During the euro debt crisis, central banks have been storing money in Treasuries and German bunds.

Another factor for the flat yields could be that investors believe the United States economy is slowing. In general, economic data has been weaker in the second quarter of this year compared with the first quarter.

“It is a barometer of what investors believe is the underpinning of the economy,” said Quincy Krosby, a market strategist for Prudential Financial, referring to the 10-year yield. “And investors are thinking the U.S economy is slowing. It should be moving higher on the back of worries in Europe diminishing, but that is not the case.”

– CHRISTINE HAUSER, New York

A few key market indicators have fluttered into positive territory, and several others are about even with their Friday close, indicating that all is not lost.

The Dow industrials are down only 6 points now, while the S.P. 500 is up a point and the Nasdaq is higher by 0.5 percent.

Even in Europe, both the FTSE 100 in Britain (up 0.3 percent) and the Dax in Germany (up 0.5 percent) have turned around. And the yield on the 10-year Italian bond has snuck below 6 percent. Spanish yields have worsened even more, however, to 7.121 percent on the 10-year.

It may be optimism. It may be profit-taking. Or it may just be the weather.

Justin Lane/European Pressphoto Agency

Justin Lane/European Pressphoto Agency

As a result of the positive but narrow Greek election, Fitch Ratings said Monday it would not change its outlook on all European government debt to negative.

Back from the brink, perhaps, Fitch said, but the crisis is still “unresolved.”

“While the risks from Greece have fallen for now, the severity of the systemic crisis engulfing the eurozone is unlikely to diminish until European leaders articulate a credible road-map that would complete monetary union with much greater fiscal and financial integration,” the credit rating company said.

The oft-cited suggestion that Greece will ask to renegotiate the terms of its bailout for more leniency could prompt other loan recipients to press for better terms, too.

However, the Irish government played down suggestions Monday that it was about to receive concessions over its international bailout following a media report in Ireland that the length of its loans might be extended.

In a statement to the media, the Irish Finance Ministry said that last July it had already obtained a concession to extend loan terms up to 30 years.

“The government is actively seeking to enhance the terms of the E.U./I.M.F. program and we will consider any proposals in this regards,” said the statement. “However, no proposals have been received from the troika along the lines reported in the media at this point.”

– STEPHEN CASTLE, London

Reuters reports that President Obama will hold a bilateral meeting with Chancellor Angela Merkel of Germany during the Group of 20 meeting in Mexico on Monday afternoon, a White House official said.

Mr. Obama is eager for Germany to guide the euro zone toward a solution to its debt crisis, which is threatening the world economy and his re-election chances, Reuters says.

And they’re off…. The Standard Poor’s 500-stock index, a broad gauge of market activity, lost 0.6 percent at the start of trading. The Dow Jones industrial average, down 65 points, and the Nasdaq composite index did likewise.

The CBOE Volatility Index, fondly known as the Vix, gained 0.7 percent.

“You can expect a little bit of a see-saw today, but a lot of it is going to be a little bit of a waiting game” for the policy committee of the Federal Reserve to meet Tuesday, said Bill Stone, the chief investment strategist for PNC Asset Management Group.

Noting the high yields on Spanish government bonds, he added, “We still sit there with plenty of things to worry about in Europe.”

– CHRISTINE HAUSER, New York

A half-hour before Wall Street clangs awake, it looks like markets-as-usual – thin volume, rocky trading and little faith in Europe. The Dow futures are down about 70 points, a perfect reversal from the 70-point-plus gain late Sunday. Spanish bond yields are still sharply (for bonds) over the troublesome 7 percent mark, and the euro has weakened a little to $1.2597. Oil and gold are lower.

Markets have now returned to fretting over the macro picture. Mark Scott reports from London that the Greek election outcome was the best of a number of bad scenarios, but that doesn’t change the fact that Spain’s unemployment is higher, bondholders may be hit as part of the 100 billion euro bailout, and growth remains sketchy. Attention is also focused on the meeting of Angela Merkel, chancellor of Germany, with the leaders of France, Spain and Italy on Friday, with some traders hoping that pro-growth measures will be announced.

“Spain poses as big a risk to markets as Greece does if it were to exit the euro,” said Pavan Wadhwa, head of global interest rate strategy at JPMorgan in London. “Nothing has really changed. Spain still has underlying growth problems and high unemployment.”

Mike Lenhoff, chief strategist at Brewin Dolphin in London, said: “Everyone knows that Germany won’t end its approach to fiscal austerity. But the markets want reassurance that there are efforts to increase growth. They want to see a pro-growth agenda before investors will be more optimistic. A singular focus on fiscal austerity just won’t do.”

The stage moves from Athens to Los Cabos, Mexico, later Monday, when the Group of 20 leading economies meets. The leadership of the European Union, which was largely in transit to Mexico while the Greek results were being made official, was still planning a news conference at 10 a.m. local time. It is to be led by Herman Van Rompuy, the president of the European Council, the body that represents European Union heads of state and government; and José Manuel Barroso, the president of the European Commission, the union’s executive agency. Analysts do not expect any firm action out of the two-day gathering.

Alexandros Vlachos/European Pressphoto AgencyAlexis Tsipras, center, entering the Greek Parliament on Monday.

Alexandros Vlachos/European Pressphoto AgencyAlexis Tsipras, center, entering the Greek Parliament on Monday.

Alexis Tsipras, whose party Syriza came in second in Greece’s election, spoke with the leader of the winning New Democracy party on Monday and later reiterated that he would refuse to join a coalition.

Mr. Tsipras, whose party had surged on a wave of anti-austerity sentiment, said he told Antonis Samaras, the New Democracy leader, that Syriza would take on “the role of a strong and responsible opposition” and “intervene in a powerful way.” Mr. Samaras is now left to construct his coalition government from among the other parties.

Updated | 8:18 A.M.

“I didn’t hear from his lips yesterday any reference to renegotiation, I only heard vows to honor commitments, to honor signatures,” Mr. Tsipras said, referring to Mr. Samaras’s victory speech on Sunday night. He said he told Mr. Samaras that there could be no more cuts to salaries and pensions, saying this would be “catastrophic” for the country.

Mr. Tsipras added that Mr. Samaras should waste no time in forming a government, saying that if he were in his position, “we would not waste a minute,” and adding that the next 10 days – ahead of a European Union summit meeting – were critical.

He added that he was certain Syriza would be vindicated in its opposition to Greece’s debt deal. And he called on all political parties to join forces in fighting an increase in violent attacks, an apparent reference to the extreme right-wing Golden Dawn party, whose members have been implicated in a growing number of assaults.

Updated | 8:24 A.M.

After his talks with Mr. Tsipras, Mr. Samaras stressed the need to renegotiate the bailout conditions. A change in policy is self-evident, he said.

— NIKI KITSANTONIS, Athens

From an initial spurt of 75 points late Sunday, the Dow Jones industrial average futures are now down about 31 points. While not pointing to a rout at the opening – at this point – that’s still 100 points more negative from where traders were soon after the Greek results were announced.

In a reminder that European policy makers remain deeply divided on how to respond to the crisis, the German Bundesbank on Monday underlined its opposition to plans to create common debt, often known as euro bonds.

The argument in favor of euro bonds is that they would leverage the good credit ratings of countries like Germany and lower borrowing costs for countries like Spain and Italy, and give those countries more time to fix their economic problems.

But, in its monthly report, the German central bank said that euro bonds would be possible only after euro zone countries have formed a fiscal union with power over the budgets of member nations, something that is years away at best. The Bundesbank also rejected a plan by the German Council of Economic Experts, an official advisory panel, for nations to pool their excess debt in a fund that would be paid off over 20 years.

Debt guaranteed by all euro zone members in common “would substantially throw off the balance between liability and control,” the Bundesbank said.

Opposition from the Bundesbank makes it more difficult for German Chancellor Angela Merkel to support a form of euro bonds, a step some analysts see as a crucial tool to end the crisis.

— — JACK EWING, Frankfurt

Bank analysts are weighing in on the Greek election, and their fairly pessimistic views may be contributing to the speed with which the market rally Monday morning has lost steam.

Many analysts predicted that the so-called troika — the International Monetary Fund, the European Union and the European Central Bank — will give a new Greek government more time to cut government spending and perhaps spread out interest payments on its debt.

“But,” Commerzbank economists said in a report Monday, “of course the Greek drama is far from over. After all, it remains to be seen whether the government will be able or willing to adhere to the watered-down conditions.

“Greece will not be out of the woods until the deficit has fallen well below 3 percent and the reforms have started to bear fruit,” the Commerzbank analysts wrote. “Until then, a renewed escalation of the Greek crisis could happen at any time, possibly ending with the country exiting monetary union.”

In a separate note, Commerzbank analyst Rainer Guntermann expressed concern that the victory of New Democracy could take pressure off euro zone leaders to deal with the larger flaws in the structure of the euro zone.

“The risk is that this benign outcome could inhibit a bolder solution at the upcoming E.U. summit,” Mr. Guntermann wrote. The summit is June 28-29.

In its European Economics Daily, Goldman Sachs said the election would offer relief for markets, but added: “This does not mean, however, that the uncertainty surrounding Greece has been resolved. Severe economic tensions combined with fierce parliamentary opposition will likely destabilize the current government in the medium run.”

Analysts at HSBC came to a similar conclusion.

“The fact remains that the challenges facing Greece are still huge,” HSBC said in a note, “and with the economy still mired in recession and the debt stock still very high, solvency concerns will persist. Hence this election outcome is unlikely to put the prospect of euro exit for Greece on the backburner for long.”

— — JACK EWING, Frankfurt

We thought that when Prime Minister Panagiotis Pikrammenos, head of Greece’s caretaker government, tried to resign earlier Monday that he had forgotten that the law dictated he stay until a new government is sworn in. But it’s part of the Kabuki theater of Greek government changeovers: the prime minister tries to resign, the president rejects the resignation and tells him he has to stay until a new government assumes office.

— NIKI KITSANTONIS, Athens

Yorgos Karahalis/Reuters, via BloombergAntonis Samaras, left, and Karolos Papoulias on Monday.

Yorgos Karahalis/Reuters, via BloombergAntonis Samaras, left, and Karolos Papoulias on Monday.

Conservative New Democracy leader Antonis Samaras visited President Karolos Papoulias to receive the mandate to form a government. In a televised exchange before their meeting, the conservative said he would approach “all parties that believe in the country’s European future” to join a “government of national salvation.”

“National consenus is the duty of all, I believe there is scope for a solution,” Samaras said. He added that he would seek “necessary changes to the program,” a clear reference to his stated aim to renegotiate some of the terms of Greece’s debt deal with foreign creditors. He added that “people must emerge from the torturous situation of unemployment and recession.”

The president, for his part, emphasized the need for the swift formation of a coalition. “The country cannot remain ungoverned even for one hour,” he said, and wished Samaras good luck in his exploratory talks with party leaders. “I am certain that national interest and national duty will prevail,” he said.

At 2 p.m. Samaras is to meet Alexis Tsipras, the leader of the radical left Syriza party, who came in second and who has already ruled out joining a coalition. Samaras is to meet the leader of Democratic Left, Fotis Kouvelis, at 6 p.m. A meeting between Samaras and Pasok leader Evangelos Venizelos — his most likely coalition partner — has not yet been scheduled (Yesterday Venizelos said yesterday that Syriza should be part of a broader coalition.).

— NIKI KITSANTONIS, Athens

Optimism in the European financial markets quickly turned to sour as traders returned to work after the Greek election.

Stock markets in Europe’s largest countries started Monday on the front foot, but soon gave away their gains as investors reacted cautiously to the weekend events in Greece and a negative report about bad debts at Spanish banks.

Stocks in Europe’s major financial markets opened the day strong, with German, French and British stocks all rising more than 1 percent in the first hour of trading.

Those gains, however, were quickly lost. The FTSE 100 index was down 0.1 percent by midmorning, while France’s CAC 40 index was trading around the same levels as Friday’s closing prices. German stocks were the only ones to hold onto their gains, though the German DAX index was up less than 1 percent in morning trading.

Analysts at Deutsche Bank said the markets already had priced in much of Monday’s share-price movements in late trading last week. The volatility also highlighted ongoing concerns in peripheral euro zone markets, particularly Spain, which did not benefit from the morning’s market increases.

Spanish stocks fell 1.67 percent in early morning trading, and shares in both Banco Santander and BBVA, the country’s largest banks, were trading in negative territory.

The Greek election result “is likely a short-term positive but we could be here again at some point in the future,” Deutsche Bank analysts Jim Reid and Colin Tad said in a report to investors. “As it is, the Greece and European relationship hobbles on crutches with many difficult challenges ahead for both parties in the coming weeks months.”

The pessimism in European markets contrasted with rises in Asia, where the news of New Democracy’s victory in the Greek election was well received. Tokyo stocks rose 1.7 percent, while shares in Sydney were 1.9 percent higher by the close of trading.

The relief also was short-lived in the currency markets. The euro, which had continued to lose its value in the last month as investors dumped the currency because of fears that Greece could leave the currency union, initially rose against other major currencies. But after stocks began to fall, the euro also gave up most of its gains, rising around 0.1 percent against the dollar, to $1.2645, in midmorning trading.

Fears put pressure on European government bonds too. Yields on Italian and Spanish sovereign debt, which had hit near record levels last week in the build up to the Greek election, fell briefly, but then jumped higher on ongoing fears about the health of the two economies.

Yields on Spanish 10-year government debt rose to 7.12 percent in midmorning trading, while Italian 10-year government bonds also were trading up, at 6.05 percent.

— MARK SCOTT, London

Antonis Samaras, head of New Democracy, meets with Greek president.

Prime Minister Panagiotis Pikrammenos, head of Greece’s caretaker government, told President Karolos Papoulias that he was submitting his resignation, a hasty move as Greek law dictates that a government remain in place, with the prime minister at its head, until a new one is formed and sworn in. “You have to stay until we have a new government, then I will release you from duty,” the president told him.

— NIKI KITSANTONIS, Athens

Reuters reports German government officials are contradicting foreign minister’s statement that Greece will be given more time to meet the troika’s deadlines.

“This just confirms that the crisis has moved beyond Greece,” Charles Diebel, head of market strategy at Lloyds Banking in London, said. “Unless we get a whole new support system, things like banking union and joint euro bonds, the peripheral countries are going to remain under pressure.”

With Spain facing borrowing costs of more than 7 percent on 10-year debt, the government is “technically insolvent” now, Mr. Diebel said. If yields remain elevated, he said, Spain will have little choice but to seek a full bailout from the International Monetary Fund, European Union and European Central Bank.

“We probably shouldn’t panic at these levels” of interest rates on Spanish debt, Mr. Diebel said, “but the market is effectively saying ‘we have no confidence in the resolution process’ ” for faltering euro members.

Mr. Diebel said it was unlikely that the Group of 20 meeting on Monday would result in any dramatic news, but that there were signs that European Union leaders meeting in Brussels at the end of June were now prepared to take bolder action than previously.

“The question, of course,” he said, “is do they have that much time.”

— DAVID JOLLY, Paris

The socialist Pasok party, which placed third in the Greek elections and would be a crucial partner in a coalition with conservative New Democracy, issued a statement saying that Prime Minister Mario Monti of Italy, who is at the G-20 summit meeting in Mexico, contacted its leader, Evangelos Venizelos, on Monday to discuss the election results and prospects. To go from leading party to third place has been a bitter pill for the socialists.

— NIKI KITSANTONIS, Athens

The European market rally appears to be losing steam, with stocks up about 0.7 percent in the euro zone, and the euro now trading at $1.2678 — still up but well off its earlier highs.

Perhaps more worrisome, Spanish 10-year bonds, which have been the focus of intense scrutiny even before the country won a 100 billion euro ($125 billion) banking sector bailout, are falling. The yield, which moves in the opposite direction of the price, rose 7 basis points to 6.87 percent. Italian 10-year bonds are trading to yield 5.94 percent, up 4 basis points.

One bond that is doing well is the Greek government 10-year, for which the yield has plummeted 85 basis points. Unfortunately, with the yield currently at 24.80 percent, the Greek sovereign debt has priced in a very high risk of default, and is largely a toy in the hands of speculators. Shares in Greek banks, meanwhile, are 15 percent higher, leading the Athens market up.

— DAVID JOLLY, Paris

Panagiotis Pikrammenos, prime minister in Greece’s current caretaker government, is to visit President Karolos Papoulias at noon in Athens (11 a.m. CET; 10 a.m. London time). Normally the prime minister visits the president in order to resign, but in this case, it’s protocol; the prime minister will not resign because the caretaker government must remain in place until a new one is formed and sworn in.

Antonis Samaras, the leader of the center-right New Democracy party, is expected to visit President Karolos Papoulias of Greece later Monday to receive a mandate to try to form a government. The time for the meeting has not yet been announced. The interior minister of the caretaker government, Antonis Manitakis, first must announce to the Parliament speaker, Vyron Polydoras, the official results of the elections. This will set off the process of asking party leaders to take the mandate from the president to try to form a coalition. (This announcement was scheduled for 10 a.m. local time — 38 minutes ago —but hasn’t happened yet.)

— NIKI KITSANTONIS, Athens

One word is dominating German news early Monday: relief.

Many major German dailies and morning talk shows all led with the Greek vote — the leading public television channel was carrying live analysis from Athens and interviews with lawmakers from New Democracy, reflecting Germans’ level of interest in the outcome.

Still, caution tempered the mood, reflecting German awareness that the Greek vote was only the first step in what will still be a long process of reform in the country — and Europe as a whole — if the Continent is to return to financial stability.

Steffen Kampeter, a deputy to the German finance minister, Wolfgang Schäuble, underlined the expectation from Berlin that a new Greek government would uphold its commitments to Europe and the euro zone. In an interview with ARD public television, he called the outcome a “chance for Greece to return to growth and stability.”

— MELISSA EDDY, Berlin

Frankfurt and Paris are immediately up 1 to 2 percent, as futures suggested.

After a bounce in Asia overnight, European financial markets are expected to follow, though the mood is one of relief rather that euphoria.

“Is euphoria appropriate in these circumstance? I wouldn’t say so,” said Kenneth Wattret, chief euro zone economist at BNP Paribas in London, “but there is relief because the election outcome could have been more problematic.”

He continued:

“In the Forex market I would expect the period of risk aversion to start to recede and, at least for a period of time, I would expect sovereign risk premiums to come down.

“But the question is how long that lasts. We have been in this crisis for some time and markets have got used to something positive happening and then enthusiasm starts to wane.

”You are betting on the ability of the Greek politicians to form an effective coalition government, and making a judgment on the leeway there is to renegotiate their program. It is pretty obvious that the current arrangements require adjustment but there is a balance between what Greece wants and what the other member states will accept.”

— STEPHEN CASTLE, London

The Greek election may be over, but the battle of the investment banks to pronounce market-defining wisdom has just begun.

Citigroup popularized the term ‘Grexit’ under its very opinionated and very much listened-to chief economist, Willem Buiter — shorthand for the idea that Greece was doomed to leave the euro, and the catchy moniker has now entered the global lexicon.

In a note today Citi economists declared the Greek election result a Pyrrhic victory and did not waver from their bearish take that Greece will be forced to exit the euro sooner than later, arguing that with the leftist Syriza party a newly empowered opposition, the ability of the new government — in whatever form it may evolve — to push through more painful spending cuts will be limited.

Here is an excerpt:

With this in mind, our probabilities for Grexit remain unchanged in the range between 50% and 75% over the next 12 to 18 months. While the outcome of the election, and the likely agreement on an ND-led government has reduced the risk of an exit in the very near term, with the large role of SYRIZA in Parliament and its power to organize protest against further austerity measures and far-reaching structural reforms on the streets, it looks to us unlikely that Greece will be able to fulfill only slightly amended conditions of the MoU.

Barclays has offered a more measured outlook.

Its analysts point out that the New Democracy victory and the ensuing coalition government will be given every opportunity by Europe to succeed and that a near-term Greek departure from currency union seems more far-fetched than ever at this moment.

Here is their take:

Pre-election, polls were showing ND and Syriza neck and neck, but in recent days the markets had probably moved to expect a ND win. As such, the results appear close to what the markets had been expecting, in our view. The fact that ND has won the most votes will be viewed as market friendly because it reduces the likelihood of a near-term Greek exit from the euro area, and will be viewed as making successful negotiations with the Troika somewhat more likely. Already on Sunday night euro area officials and the IMF have expressed their willingness to look at adjusting some elements of the programme, in particular its timing. Overall, however, we expect the effect on the EUR and risky currencies and assets to be muted.

What does seem certain is that investors will heave a short term sigh of relief that their worst nightmare of a large Syriza victory did not materialize — as some private and early pre-election polls were predicting. But, while there may be a relief rally — as buoyant Asian markets are now showing — attention will soon turn from Grexit musings to the more pressing topic of whether Spain and Italy can keep raising money from increasingly jittery bond investors.

— Landon Thomas Jr.

European markets are expected to react with glee at the victory of the pro-bailout New Democracy party in Greece. But the win of an outright majority by France’s Socialists will likely be viewed negatively by markets.

European markets futures point to a strong opening. No surprise there, of course. Frankfurt opening in an hour. How long will the relief rally last, though, and what will we look like by the end of the day?

The Greek daily Kathimerini has the near-final tally of Sunday’s vote.

Eirini Vourloumis for The New York TimesVillagers in Touthoa, Greece, waiting for their results to be announced on Sunday.

Eirini Vourloumis for The New York TimesVillagers in Touthoa, Greece, waiting for their results to be announced on Sunday.

In one Greek village, voters reckoned with decades of decisions that led to the nation’s current troubles, Liz Alderman reports:

Far from the grim atmosphere gripping Athens, Touthoa teems with silver-tipped olive groves, sun-kissed vegetable gardens and flocks of sheep, living testaments to the centuries-long natural wealth of this resilient nation.

It would seem easy for residents here to feel removed from the crisis that has racked the seat of government since the last elections, on May 6, left a vacuum in Greece’s leadership and threatened the country’s future within the euro monetary union. More than half of Greece’s 11 million people live outside big cities, many in rural towns like this one.

But the generations of families that gathered Sunday in Touthoa, founded by the ancient Greeks on a limestone cliff along a mythic river by the same name, were far from disengaged.

Keith Bradsher reports from Hong Kong:

Stock markets in Hong Kong and mainland China rallied on Monday morning along with other Asian markets while the Chinese central bank set an initial trading value for the renminbi on Monday morning that was 0.13 percent higher than on Friday. But Greece’s financial troubles remain a considerable worry for Chinese policymakers.

“The Greek election results unfortunately don’t seem to offer any clarity on the policy measures needed to keep Greece in the Eurozone and stabilize its public finances,” said Fred Hu, a prominent Chinese economist who has advised Chinese economic policymakers for years and is now the chairman of Primavera Capital, a Beijing-based private equity firm. “The last thing investors need is heightened political uncertainty and policy paralysis, which has gripped Greece.”

The Hang Seng Index rose 1.6 percent in early trading in Hong Kong on Monday while the Shanghai stock market was up 0.5 percent.

Chinese exports to Europe have stagnated this spring, as wholesalers and retailers there have been reluctant to commit themselves to large orders while waiting to see whether European economies will weaken further. The Chinese government has teams of experts working on contingency plans if Greece does leave the euro.

“China watches the developments in Europe with deep concern and resignation,” Mr. Hu said. “The intensifying crisis in Europe has hurt confidence and threatened global economic recovery. China hopes that Europe can unite and take decisive actions together to contain the crisis.”

President Hu Jintao, in a written interview with a Mexican publication before the G-20 meeting in Mexico on Monday and Tuesday, called for improved international economic cooperation. He particularly endorsed the implementation of various changes at the International Monetary Fund – where China is seeking greater voting rights at the expense of European nations that represent a dwindling share of global economic output – and the completion of the Doha Round of global trade talks.

While investors may have been relieved by the outcome of the elections in Greece on Sunday, larger concerns about the structural problems throughout southern Europe remain, The Times’s Nathaniel Popper reports:

“Unless they make a radical change, we will be back with another Greek cliffhanger in three or four months’ time,” said Darren Williams, a European economist at AllianceBernstein in London.

What is more, economists remain concerned about the debt and banking crises in several larger European nations, including Spain and Italy. These issues will take center stage at a series of coming international political gatherings, including a meeting of the Group of 20 nations that is set to begin on Monday in Mexico.

Later in the week, the leaders of the four largest European economies will meet to begin discussing ways to stimulate growth on the Continent while still shrinking budget deficits and debts.

Investors question whether European leaders can achieve the type of increased fiscal and political integration viewed as necessary to keep the Continent’s common currency alive.

Specifically, some European leaders have called for some kind of guarantee on bank deposits throughout the euro zone, which would help stop the flight of capital from banks, and for the European Central Bank to have the ability to issue euro zone bonds to help spread risk away from troubled borrowers like Spain and Italy.

Hiroko Tabuchi reports from Tokyo:

Securities firms, which had been bracing for market turmoil in the wake of the Greek elections, led a rally in the Nikkei 225 Stock Average, bringing it to its highest level since mid-May. Nomura Holdings, rose 3.32 percent and the camera maker Canon, which sells a third of its cameras in Europe, rose 2.97 percent.

Japan’s pro-austerity prime minister Yoshihiko Noda scored his own victory on Friday, striking a deal with the opposition to introduce a consumption tax unpopular with voters that would help Japan pay for its burgeoning social welfare costs.

Nicholas Smith, a Tokyo-based equity strategist, warned in a note to clients that to placate an divided public, austerity measures in Greece, Japan and elsewhere needed to be followed by strong steps to grow the economy.

“Short-term, it will cause a relief rally, but that may well be at the expense of medium-term growth unless the Old Testament wrath brought down on Greece can be offset by pro-growth measures elsewhere,” he said. “Unfortunately, every time they practice austerity they seem to increase the budget deficit by crushing the economy.”

Neil Gough reports from Hong Kong:

Global markets are breathing a sigh of relief at the result of Greek elections, with most Asian share indexes rising Monday morning.

Japan’s benchmark Nikkei share index and the Kospi index in South Korea both were sustaining increases of around 2.1 percent an hour into their trading day. Australia’s SP 200 index was up 1.7 percent. The Japanese yen fell against the United States dollar in morning trading, while the Australian dollar rose.

Asian markets have been roiled this year by the ongoing debt crisis in Europe, a major trading partner to export powerhouses like China and Japan.

The Nikkei had fallen nearly 20 percent from late March to a low of 8,295 points in early June, but Monday’s gains have helped add to a recent rebound that has seen the Japanese blue chip index rise by more than 5 percent in the last two weeks.

Still, market volatility remains elevated, and is unlikely to diminish despite the victory by Greece’s main pro-bailout party in Sunday’s vote.

In Hong Kong, the Hang Seng Volatility Index, which attempts to measure near-term future fluctuations in the city’s benchmark share index, had been steadily declining all year. But since the previous Greek vote on May 6, it soared by almost 50 percent, to 28 index points as of Friday.

From Melissa Eddy in Berlin:

Martin Schulz, president of the European Parliament, who was the only European official to have visited Greece between the two rounds of parliamentary elections, underlined the expectation from Brussels that any newly formed Greek government accept the basic principles of the so-called memorandum of understanding agreed to by both parties.

He recalled that in the past, Antonis Samaras has not always been supportive of the efforts to help Greece restructure its economy and remain in the euro zone. “For quite a while, Mr. Samaras refused to accept the measures with the European Union,” Mr. Schulz, who is German, told ARD public television earlier Sunday. “But I trust him to become a responsible partner.”

He stressed that Europe remains willing to help Greece, as long as Greece is willing to accept what Europe expects of it, acknowledging that it would not be easy. “The path ahead of the Greeks is difficult, but outside of the euro zone it certainly would have been even more difficult,” Mr. Schulz said.

Stocks in Japan opened higher, with the Nikkei 225 up 2.3 percent in early trading, and the Kospi in South Korea rose 2 percent. Here is a list of the opening times of stock markets around the world. Frankfurt is the earliest major European market to open, at 8 a.m. local time.

Niki Kitsantonis, reporting from Athens, reminds us that the Greek government is likely to run out of money very soon, so no one should be taking a breather based on the non-catastrophic election results.

The previous billions in bailout money that went to Greece has been spent on interest and maturing debt, she reports. While it is unclear exactly when the government’s cash flow will cease, reports leaked from a Finance Ministry meeting said July 20, and Lucas Papademos, former prime minister, warned that cash would dry up this month. And that means the government would be unable to pay salaries and pensions.

Meanwhile, Greece is being run with a caretaker government, a prime minister and cabinet, that was sworn in on May 17, after the failed May 6 elections. The president, Karolos Papoulias, is still in his post; his position is not affected.

President François Hollande’s Socialists and their allies won an absolute majority in runoff parliamentary elections on Sunday, strengthening the hand of Mr. Hollande both at home and in Europe, where he is pressing for less austerity and more growth in the face of a deepening recession. Read more »

The early money has stocks going higher in New York on Monday morning: Futures trading of the Dow Jones industrial average opened up about 75 points on Sunday. While that will change countless times before the 9:30 a.m. start of regular trading, the healthy rise shows there’s some early confidence among investors after the preliminary Greek results. And 30-year Treasury bond futures fell more than a point at the opening of electronic trading.

None of which is necessarily good news for stockholders. The slim apparent victory of the New Democracy party, the group that supports sticking with the euro, most likely means the coalition government that results in Athens will be more of the same stalemate of the past many months — European insistence on government sacrifice and austerity, followed by Greek political and public resistance to wholesale structural change. Wall Street’s reaction to that has not been exactly rousing, with the Dow up 4.5 percent since the beginning of the year.

Meanwhile, the first stock market to open in Asia, New Zealand’s, was virtually unchanged in early trading on Monday.

Binyamin Appelbaum from Washington reports:

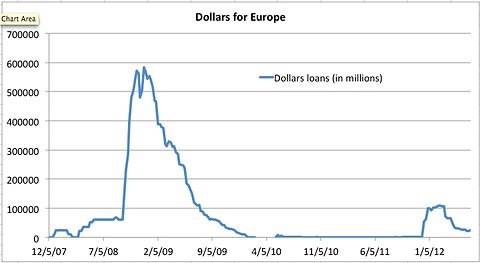

One measure of stress in the European financial system barely budged in the weeks leading up to the Greek vote. Foreign banks that run short on dollars can borrow the currency from the Federal Reserve through their own central banks. The volume of those loans has tended to climb sharply during periods of financial stress.

The chart below shows the volume of loans since the program began in 2007, with the heaviest use during the depths of the financial crisis and a smaller peak earlier this year, when investors were concerned that Greece and its creditors would not reach their eventual agreement to restructure the country’s debts.

Federal ReserveDollars borrowed from the Federal Reserve by foreign banks, Dec. 2007 – Jun. 2012.

Federal ReserveDollars borrowed from the Federal Reserve by foreign banks, Dec. 2007 – Jun. 2012.

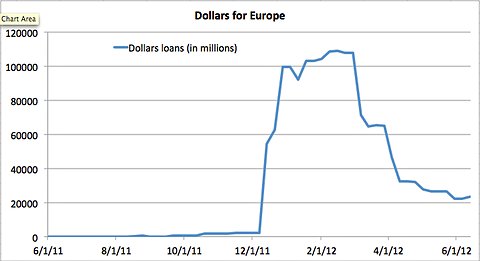

The second chart zooms in on borrowing over the last year. The volume of dollar loans peaked at $109 billion in mid-February, then gradually declined to $22.2 billion at the end of May. And over the last two weeks, the volume of loans has climbed only slightly to $23.3 billion, the Fed reported Thursday.

Federal ReserveDollars borrowed from the Federal Reserve by foreign banks, Jun. 2011 – Jun. 2012.

Federal ReserveDollars borrowed from the Federal Reserve by foreign banks, Jun. 2011 – Jun. 2012.

The charts suggest that the global financial system is far from perfect health, but also far from the worst periods of crisis over the last few years. The next update from the Fed, later this week, will tell us if that begins to change.

After a 3 percent decline against the dollar since the Greeks first voted in May, the euro on Sunday is “broadly positive” at about $1.27, Bloomberg News reports. Neil Jones, the euro head of European hedge-fund sales at Mizuho Corporate Bank in London, told the news serivce, “If New Democracy get enough to form a coalition, they’ll stick to the mandate and maintain the euro which will be a big relief to markets around the world.”

Melissa Eddy in Berlin reports:

Germany’s finance minister, Wolfgang Schäuble, welcomed the preliminary results, saying it represented “a decision by Greek voters to forge ahead with the implementation of far-reaching economic and fiscal reforms in the country.”

Mr. Schäuble underlined Antonis Samaras’s pledge in February to the central measures of the bailout program that was drawn up by Europe and the Greeks in an effort to keep the country in the euro zone.

Updated | 6:16 p.m.

Angela Merkel, chancellor of Germany, called Antonios Samaras to “congratulate him on a fine result” and express the “hope for a stable government, soon,” her spokesman, Steffen Seibert, tweeted late Sunday. The chancellor had previously been scheduled to depart for the Group of 20 meeting in Los Cabos, Mexico at 8 p.m., but postponed her departure until midnight, as did Mr. Schäuble.

Srdjan Suki/European Pressphoto AgencyGermany beat Denmark at the Euro 2012 soccer championship on Sunday setting up a quarterfinal face-off with Greece on Friday.

Srdjan Suki/European Pressphoto AgencyGermany beat Denmark at the Euro 2012 soccer championship on Sunday setting up a quarterfinal face-off with Greece on Friday.

Officials in Berlin appear to be sighing in relief — and not just over the election. Germany defeated Denmark 2-1 late Sunday in the Euro 2012 soccer championship. But the best is yet to come: Germany will now face Greece in the quarter finals on Friday in Gdansk, Poland, setting the rest of the country on edge about the new threat posed by the Greeks.

From Keith Bradsher in Hong Kong:

While it looks like the chance of a departure of Greece from the euro zone is now remote, given the election results, among those that had contingency plans were Chinese government officials, which have had teams of civil servants and executives at state-owned banks conducting analyses and making preparations.

Chinese economists said that a Greek exit would create two potential worries for the Chinese economy: a likely weakening of demand in Europe, China’s biggest market for exports, and a possible worldwide flight of capital from emerging markets like China’s if a Greek exit seriously undermines global financial stability.

Yu Yongding, a top economist at the Chinese Academy of Social Sciences and a former member of the monetary policy committee at the country’s central bank, said that he was skeptical that Greece would leave the euro zone quickly, even if the leftist party Syriza had prevailed. Either side, he said, would seek a better deal from the rest of Europe before actually pulling out.

While Europe is often described as China’s biggest customer, it accounts for only a quarter of China’s heavily diversified exports. The United States almost matches the European Union as a buyer of Chinese goods, while other Asian markets and the rest of the developing world are also large customers. The long-term effect of European economic troubles on these markets is less clear.

As the euro has weakened against the dollar this spring, the Chinese government has let the renminbi also weaken against the dollar, although not as much. This has helped cushion the effect on Chinese exporters from the euro’s difficulties. Chinese overall exports rose 15.3 percent in May from a year earlier, propelled by a gain of 23 percent in shipments to the United States.

James Kanter in Brussels reports:

The leadership of the European Union plans to take a day to digest the results before holding a news conference that has been scheduled for Monday at 10 a.m. local time in Los Cabos, Mexico, where the Group of 20 is meeting. Herman Van Rompuy, the president of the European Council, the body that represents E.U. heads of state and government, and José Manuel Barroso, the president of the European Commission, the union’s executive agency, issued a statement of support on Sunday, saying, “We will continue to stand by Greece as a member of the E.U. family and of the Euro area.” They planned to speak at the Faro hotel on the sidelines of the G-20 in Los Cabos.

Binyamin Appelbaum from Washington reports:

Unless the situation in Europe deteriorates significantly, the Federal Reserve is unlikely to announce any immediate changes in policy. The Fed already offers money to American banks that need emergency loans and, since 2007, also has made dollars available to European banks that need emergency loans.

Moreover, the Fed’s policy-making committee already plans to hold a long-scheduled meeting Tuesday and Wednesday. Even if Fed officials decide the American economy needs more help, they may not see a need to rush.

That said, if the Fed did decide to act – perhaps as part of a coordinated effort with other central banks to calm global financial markets – it has options.

The central banks could simply issue a joint statement affirming their commitment to maintain the stability and function of financial markets. This amounts to stating the obvious, but in times of crisis, people take comfort in affirmations.

The Fed could extend the availability of dollar loans for foreign banks, which are offered by agreement with other central banks, beyond the scheduled sunset in February 2013. The Fed also could reduce its fee, as it did in November, when it announced a reduction from one percentage point to half a point.

It would be technically impossible to repeat the October 2008 decision by the world’s major central banks to simultaneously reduce their benchmark interest rates, for the simple reason that the Fed has held its benchmark rate near zero since December 2008. But the Fed could attempt the modern equivalent by announcing that it will expand its holdings of Treasuries and mortgage securities.

And central banks could intervene if necessary to stabilize the value of the euro. The members of the Group of 7 nations most recently intervened in global currency markets in March 2011 to stabilize the value of the yen. But policymakers regard such interventions as effective and worthwhile only if market speculation is causing a currency to deviate from its underlying value.

Rachel Donadio has the latest on the vote from Athens, where it appears the allies of the euro zone have eked out a victory.

Paul Geitner from Brussels reports:

In a statement, Greece’s partners in the Eurogroup noted the election’s provisional results, which they said “should allow for the formation of a government that will carry the support of the electorate to bring Greece back on a path of sustainable growth.”

The group of finance ministers said they expected officials from the trio of institutions supervising Greece’s second bailout program to return to Athens as soon as a new government is in place to begin discussing “the way forward.”

While acknowledging the “considerable efforts already made” by Greeks, the ministers said they were “convinced that continued fiscal and structural reforms are Greece’s best guarantee to overcome the current economic and social challenges and for a more prosperous future of Greece in the euro area.”

Nathaniel Popper in New York reports:

The euro gained in value against the dollar Sunday afternoon (New York time) in an early sign that the Greek elections could provide at least a temporary boost to global financial markets.

The early numbers coming out of Greece suggest that the New Democracy party and its mainstream partners may have enough votes to form a government and continue to receive the international aid that is keeping the country afloat.

If that outcome holds, it could avert the doomsday scenario of Greece making a sudden and messy exit from the euro currency. Such fears had driven the value of the euro down in recent weeks, but on Sunday the currency was up by 0.5 percent against the dollar to $1.2703.

While most financial markets are closed during the weekend, foreign currency trading is always open. Due to the generally light volume of weekend trading, market watchers cautioned about drawing broad conclusions from the movements on Sunday. But the euro’s tick upward was consistent with the relief expressed by strategists and investors watching the election results.

“It looks like we’ve avoided the worst case scenario,” said Darren Williams, a European economist for Alliance Bernstein in London. “I think that’s important because we could have gone to a very bad place very quickly.”

Article source: http://thelede.blogs.nytimes.com/2012/06/17/aftermath-of-the-greek-vote/?partner=rss&emc=rss

Speak Your Mind

You must be logged in to post a comment.