CATHERINE RAMPELL

Dollars to doughnuts.

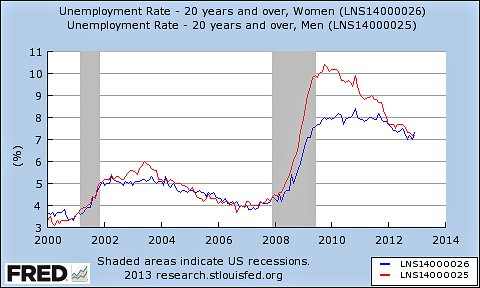

For the first time in more than six years, the unemployment rate for adult women (those over age 20), seasonally adjusted, has surpassed that for adult men.

Federal Reserve Bank of St. Louis Women’s unemployment rate is in blue, men’s in red. Data are seasonally adjusted.

Federal Reserve Bank of St. Louis Women’s unemployment rate is in blue, men’s in red. Data are seasonally adjusted.

This reversal was first noted by Joan Entmacher, vice president for family economic security at the National Women’s Law Center.

During the recession, men had borne the brunt of job losses, which were disproportionately in male-dominated industries like construction and manufacturing. Over the course of the recovery that began in mid-2009, however, these sectors have improved a little, while the female-dominated public sector has been shedding workers.

As you can see in the chart above, the unemployment rate for adult men (red line) has fallen sharply since early 2010. That trend is due in part to stronger hiring of men, but also to a more discouraging development: men are dropping out of the labor force in very high numbers.

The unemployment rate for adult women (blue line) never got nearly as high as that for men, but then it has not fallen by much either. Like men, women were leaving the labor force in droves from 2009 to 2011. Women’s participation rates appeared to stabilize somewhat last year.

I should note, by the way, that the unemployment rate for male teenagers is still much higher than that of females: 25.9 percent compared with 21.2 percent.

Article source: http://economix.blogs.nytimes.com/2013/01/04/womens-unemployment-surpasses-mens/?partner=rss&emc=rss