The stock market rose slightly on Thursday, pushing the Dow Jones industrial average to a new nominal high after it surpassed its previous peak two days ago. The gains came after a new report provided evidence that hiring was picking up.

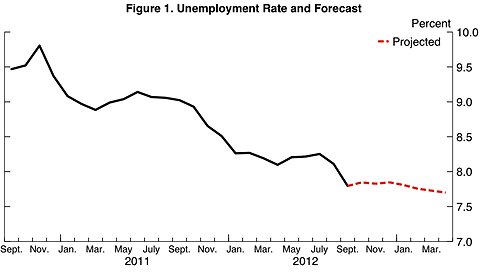

The Labor Department reported that the number of Americans seeking unemployment benefits fell by 7,000 last week, driving the four-week average to its lowest point in five years. The drop in new jobless claims is a positive sign ahead of Friday’s employment report.

The Dow industrials rose 33.25 points, or 0.2 percent, to 14,329.49. The Standard Poor’s 500-stock index gained 2.80 points, or 0.2 percent, to 1,544.26. Both indexes rose for the fifth consecutive day.

The S. P. 500 is closing in on its own high close of 1,565.15, which was reached on Oct. 9, 2007, the same day as the Dow’s previous peak. The S. P. 500 would need to rise 20.89 points, or 1.4 percent, to set a nominal record, though both indexes are still far below their peaks if inflation is taken into account.

Investors have been buying stocks on optimism that employers are slowly starting to hire again and that the housing market is recovering. Growing company earnings are also encouraging investors to enter the market. The Dow is 9.4 percent higher so far this year and the S. P. 500 is up 8.3 percent.

“If you have a multiyear time horizon, equities are an attractive asset, but don’t be surprised to see some volatility, especially after the big run we’ve had,” said Michael Sheldon, chief market strategist at the RDM Financial Group.

The Nasdaq composite index advanced 9.72 points, or 0.3 percent, to 3,232.09. It is up 7 percent this year, but it is well below its high of more than 5,000, reached during the dot-com boom in 2000.

Boeing helped lead the Dow higher on Thursday, advancing $1.97, or 2.5 percent, to $81.05 after reports that American regulators were poised to approve a plan within days to permit the company to begin test flights of its 787 Dreamliner jet. The 787 fleet has been grounded since Jan. 16 because of safety concerns about the plane’s batteries.

Jeffrey Saut, chief investment strategist at Raymond James, predicted that any sell-off in stocks might be short-lived as investors who have missed out on the rally since the start of the year jump into the market.

“The rally is going to go higher than most people think,” Mr. Saut said. “This thing has caught most money managers flat-footed.”

The stock market’s rally this year has been helped in no small part by continuing economic stimulus from the Federal Reserve, which is buying $85 billion each month in Treasury bonds and mortgage-backed securities. That has kept interest rates near historical lows, reducing borrowing costs and encouraging investors to move money out of conservative investments like bonds and into stocks.

On Thursday, however, interest rates moved higher in the bond market. The price of the 10-year Treasury note fell 16/32, to 100 2/32, while its yield rose to 2 percent from 1.94 percent late on Wednesday.

Among the stocks making big moves, PetSmart fell $4.37, or 6.6 percent, to $62.18 after the company reported its fiscal fourth-quarter earnings. Profits for the pet store chain rose, but its forecast for this year disappointed investors.

Pier 1 Imports fell 96 cents to $22.28 after the company issued an earnings forecast that was below Wall Street analysts’ estimates.

The supermarket chain Kroger rose 89 cents, or 3 percent, to $30.25 after the company’s fourth-quarter profit handily beat Wall Street expectations.

Gap rose $1.41, or 4.1 percent, to $35.87 after it said a crucial revenue measure rose more than expected in February, helped by sales at its Gap and Old Navy stores.

Article source: http://www.nytimes.com/2013/03/08/business/economy/daily-stock-market-activity.html?partner=rss&emc=rss