Chuck Burton/Associated Press Home construction this spring in Matthews, N.C., near Charlotte.

Chuck Burton/Associated Press Home construction this spring in Matthews, N.C., near Charlotte.

Home prices in the United States have been on a roller coaster ride for the last decade — soaring through 2005, then plunging in the steepest decline since the Great Depression. In 2012, though, prices began moving upward.

How solid is the incipient housing recovery, and what are the prospects for home prices in the decade ahead?

Some fresh clues about the short-term trends began arriving this week. And an analysis of the long-term prospects for home prices began appearing in a three-part series of columns in Sunday Business by Robert Shiller, the Yale economist.

First, the short-term trend: based, at least, on a report on Monday morning, it appeared to be taking a zigzag path rather than a straight line upward. According to the National Association of Home Builders/Wells Fargo Housing Market index, sentiment among home builders declined in April for the third consecutive month, to 42 from 44 the previous month. While that index climbed in 2012, it has not been above the neutral level of 50 since April 2006, when the market collapse was already under way.

Another report is due on Tuesday. That’s the Commerce Department’s tally of housing starts and building permits in March. Both numbers rose sharply in February and Wall Street economists were expecting another set of strong numbers.

The short-term trend for the housing market seemed clear and strong enough for Michael E. Feroli, chief United States economist at JPMorgan Chase, to conclude in a report on April 10 that residential investment – including homebuilding, repairs, renovation and brokers fees – would rise enough this year to add 0.5 percent to G.D.P. growth.

As for home prices, no major reports were imminent. But in the fourth quarter of 2012, the latest home period included in the Standard Poor’s Case-Shiller 20-city index, prices rose sharply, at the fastest rate since June 2006.

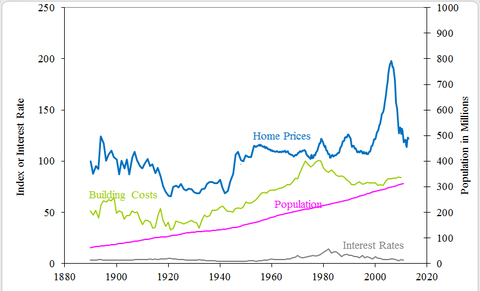

Professor Shiller, who helped devise the Case-Shiller index, says in his Economic View column on Sunday even if the upward trend for prices continues for a while, historical data shows that it’s not necessarily meaningful over the long haul.

“One-year home price increases, after correcting for inflation, have had almost no statistical relationship to increases 10 years down the road,” he writes. “Thus, the upturn last year is irrelevant to long-run forecasting. Booms are typically followed by busts, usually in far less than 10 years. In a decade, an entire housing boom, if there is one in inflation-corrected terms, is likely to have been reversed and completely washed away.”

Source: Robert J. Shiller, “Irrational Exuberance,” Second Edition (Princeton University Press), as updated by author.

Source: Robert J. Shiller, “Irrational Exuberance,” Second Edition (Princeton University Press), as updated by author.

In assessing long-term price trends, he says, prospective home buyers ought to emphasize fundamental factors like inflation and construction costs, which he discusses in his first column. While inflation creates the illusion that real home prices are increasing, rising productivity in the construction industry often drives down the cost of housing.

Next Sunday’s column will deal with real estate bubbles, and with the speculative effects of years of declining interest rates on housing and other markets. The third will consider cultural and demographic trends, including the stimulative market influence of a rising population — and the potential constraints on prices that could occur as America ages..

Article source: http://economix.blogs.nytimes.com/2013/04/15/housing-trends-short-and-long-term/?partner=rss&emc=rss

Speak Your Mind

You must be logged in to post a comment.