Casey B. Mulligan is an economics professor at the University of Chicago.

The combination of housing market events and the profit motive of mortgage lenders turned trillions of dollars of household debt into a huge safety net.

Today’s Economist

Perspectives from expert contributors.

Household debt had been increasing during the 1980s and 1990s, but the rate of increase was extraordinary in the years leading up to the recession. By 2007, household sector debt had reached 114 percent of the nation’s personal income – more than $14 trillion. The change was almost entirely due to accumulation of home mortgage debt.

Normally, home mortgages are fully secured by a residential property, and when a homeowner fails to make the scheduled payments on time, the lender can seize the property and sell it to recover its principal, interest and fees. When the lender has this valuable foreclosure option, borrowers overwhelming either make their home mortgage payments on time or sell their property in an orderly fashion to obtain the money to repay the mortgage lender, even in cases when the homeowner is unemployed.

When residential property values plummeted in 2008 and 2009, a number of residential properties were suddenly “under water” — worth less than the mortgages they secured. In those cases, the lender’s foreclosure option was no longer valuable – selling the property would be likely to yield too little money to cover principal, let alone interest and fees.

Lenders needed a way to estimate which borrowers would still pay in full and a way for other borrowers to work out a mortgage modification that would give them an incentive to pay at least a bit more than their homes were worth.

Naturally, a borrower’s income is a factor considered – borrowers with high income can be expected to repay more than borrowers with low income. Thus, a partial solution to the lenders’ collection problem is to insist that high-income borrowers pay more of the mortgage amount due and allow at least some low-income borrowers to pay less.

From this perspective, the lenders’ desire to maximize debt collections (after the collapse of residential real estate values) causes them to create a kind of safety net program that gives low-income people more help with their housing expenses (much the way the federal food stamp program gives low-income people more help with their food expenses) in the form of modified mortgage payments.

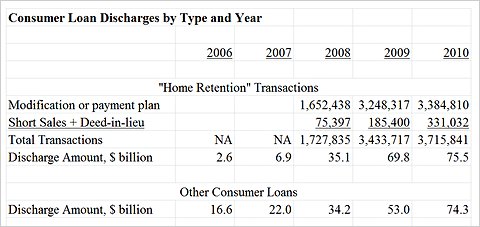

To quantify the size of the loan modification safety net and its changes over time, I estimate the amounts that “home retention actions” (as the federal government calls these mortgage modifications that allows people to stay in their homes) actually changed mortgage payments from the original mortgage contract, which specified only payment in full or foreclosure.

To estimate those amounts for 2008-10, I first measured the number of residential properties in each quarter receiving loan modifications, lender permission for short sale or lender permission for deed-in-lieu of foreclosure.

Next, I multiplied the number of transactions by a $20,319 average value of each loan modification (a typical modification reduced monthly payments by $400 for a minimum of 60 months; at an annual discount rate of 7 percent, that’s a present value of $20,319). I do not have data on the number of home retention actions for the years 2006 and 2007, but I assume the dollar value of discharges those years were, as a proportion to discharges in 2008, the same as total mortgage loan discharges by commercial banks.

Because the home retention actions are necessary primarily when homes are worth less than the mortgages they secure, the amount discharged by home retention actions is much less in 2006 and 2007 when residential property values were still high. During 2010, mortgage lenders discharged more than $70 billion of mortgage debt through home retention actions. Seventy billion dollars for one year is small in comparison to the total amount that homeowners were under water but is more than the spending by the entire food stamp program for that year.

The last row of the table displays discharges on other consumer loans, such as credit card debt. Those discharges are smoother over time because they are not directly tied to the housing cycle but still totaled more than $70 billion in 2010. The combination of discharges of other consumer loans and discharges of home mortgages by home retention actions was almost $150 billion in 2010, which exceeds the peak spending for entire unemployment insurance system.

Bankers deserve a lot of blame for getting us into this mess, have dipped far too deeply into the United States Treasury to help themselves, and have been far too slow to modify mortgages. For these reasons, it’s remarkable that their own selfish pursuits have forced them to create a safety net of sorts that rivals the amounts spent by public sector safety net programs.

Article source: http://feeds.nytimes.com/click.phdo?i=f0a9e27a51ba4d0f9f582cf3a628574f

Speak Your Mind

You must be logged in to post a comment.