For those of you wondering if you’re saving enough money for retirement, here are some new savings guidelines to ponder.

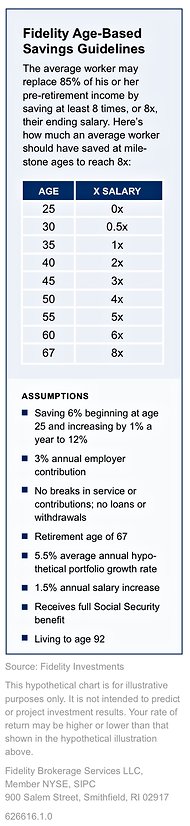

Fidelity Investments has recommended that most workers should strive to save at least eight times their final salary before they retire to adequately prepare for retirement. (Saving that amount puts you on track to replace 85 percent of your salary, Fidelity says.)

Now, the investment firm is suggesting earlier milestones to help you get to that eight times goal by the time you’re 67.

Namely, Fidelity suggests workers should aim to save about one times their salary at age 35, three times at age 45 and five times at age 55.

So if you’re 45 and you’re making $50,000 a year, you should have put away $150,000.

“We believe these savings targets offer a rule of thumb to help employees get engaged in retirement planning by making it simpler and more achievable, but we recognize many individuals may need more than eight times their ending salary in retirement based on their lifestyle,” James M. MacDonald, president of workplace investing at Fidelity, said in a news release.

The company’s savings guideline is based on an employee in a workplace retirement plan, like a 401(k), beginning at age 25, working and saving continuously until age 67 and living until age 92. The goal would include savings in all retirement accounts, like 401(k)’s and I.R.A.’s, as well as other savings.

The calculation includes several assumptions, like a lifetime average annual portfolio growth rate of 5.5 percent and income growth of 1.5 percent a year over inflation with no breaks in employment.

So, all of you out there who are 35, 45 and 55(ish), are you anywhere near those targets? How did you do it?

Article source: http://bucks.blogs.nytimes.com/2012/09/12/suggested-retirement-savings-goals-by-age/?partner=rss&emc=rss

Speak Your Mind

You must be logged in to post a comment.