CATHERINE RAMPELL

Dollars to doughnuts.

One of the more unsettling trends in this recovery has been the rise of part-time work.

We are nowhere near recovering the jobs lost in the recession, and the track record looks even worse when you consider that so many of the jobs lost were full time, whereas so many of those gained have been part time.

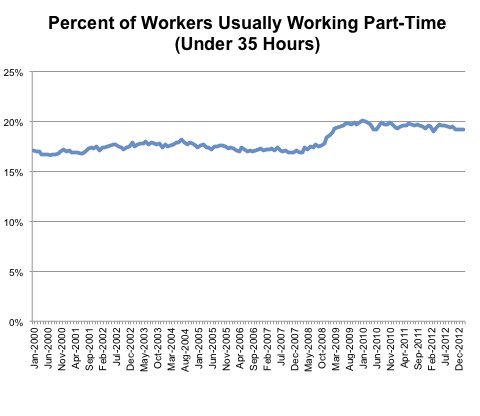

Compared with December 2007, when the recession officially began, there are 5.8 million fewer Americans working full time. In that same period, there has been an increase of 2.8 million working part time. Part-time workers — defined as people who usually work fewer than 35 hours a week — are still a minority of the work force, but their share is growing.

Source: Bureau of Labor Statistics, via Haver Analytics.

Source: Bureau of Labor Statistics, via Haver Analytics.

When the recession began, 16.9 percent of those working usually worked part time. That share rose sharply in 2008 and 2009 and has not fallen much since then. Today the share of workers with part-time jobs is 19.2 percent.

This would not be so troubling if people were electing to work fewer hours. But that is not the case.

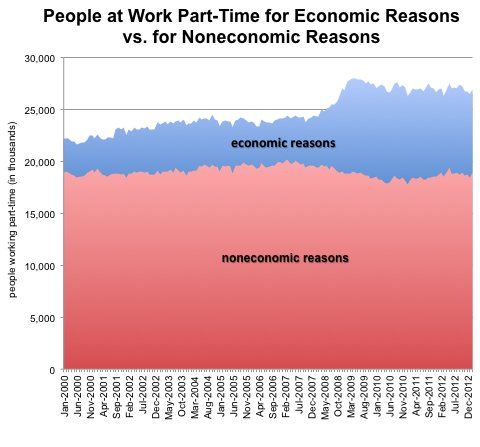

Basically all of the growth in part-time workers has been among people reluctantly working few hours because of either slack business conditions or an inability to find a full-time job. Together these people are considered to be working part time “for economic reasons.” Their numbers have grown by 3.4 million since the downturn began.

The number of people working part time “for noneconomic reasons,” on the other hand, has fallen by 639,000 since the recession began.

Source: Bureau of Labor Statistics, via Haver Analytics.

Source: Bureau of Labor Statistics, via Haver Analytics.

These trends are part of the reason that many people believe the standard unemployment rate of 7.7 percent understates the extent of underemployment. If you include both part-time workers who want full-time work and people who have stopped looking for jobs but still want to work, the unemployment rate is actually 14.3 percent.

It’s not clear what’s behind the growth in part-time work. It probably has to do mostly with companies’ not having as much need for labor today as they did when the economy was strong. The Affordable Care Act also has incentives for employers to keep their count of full-time workers below 50, but that has probably affected only a few companies at the margin at this point.

Article source: http://economix.blogs.nytimes.com/2013/03/08/the-rise-of-part-time-work/?partner=rss&emc=rss